These stocks raised their dividends annually for at least a decade and should continue rewarding investors for years.

While high-yield dividend stocks may attract outsized attention from investors, companies paying well-funded and growing, albeit smaller, dividends tend to outperform the market and their peers over the long term. Three companies that encapsulate this market-beating potential are Visa (V 1.17%), FactSet Research Systems (FDS 0.68%), and Nasdaq (NDAQ) -11.81%), which have posted total returns of over 400%, 300%, and 500% in the last decade, respectively. By maintaining payout ratios below 30%, these stocks’ dividend payments are well-funded and primed to continue increasing for decades.

These three businesses are in leadership positions in their niches. Let’s explore why they’re perfect for investors looking to grow their passive income throughout the rest of their lives.

1. Visa

While payments behemoth Visa and its 0.8% dividend yield may not immediately shout “massive passive income potential” at investors, its 17% annualized dividend growth rate over the last five years highlights its compounding nature.

Having grown its annual per-share dividend payments from $0.11 in 2010 to $2 currently, Visa has continued its market-crushing ways, rewarding shareholders along the way.

So what exactly makes the company interesting at this moment in time?

Management identified three unique growth levers to pull in consumer payments, new flows (think business-to-business payments or remittances), and value-added services. The company’s upcoming rollout of Visa+ — an interoperable peer-to-peer (P2P) payment offering — looks particularly interesting, bringing a partnership with PayPal, Venmo, and others to the masses.

By opening up the closed-loop worlds of the growing number of P2P networks and digital wallets, Visa+ could finally link all these disparate solutions, doing what the company does best — joining networks together.

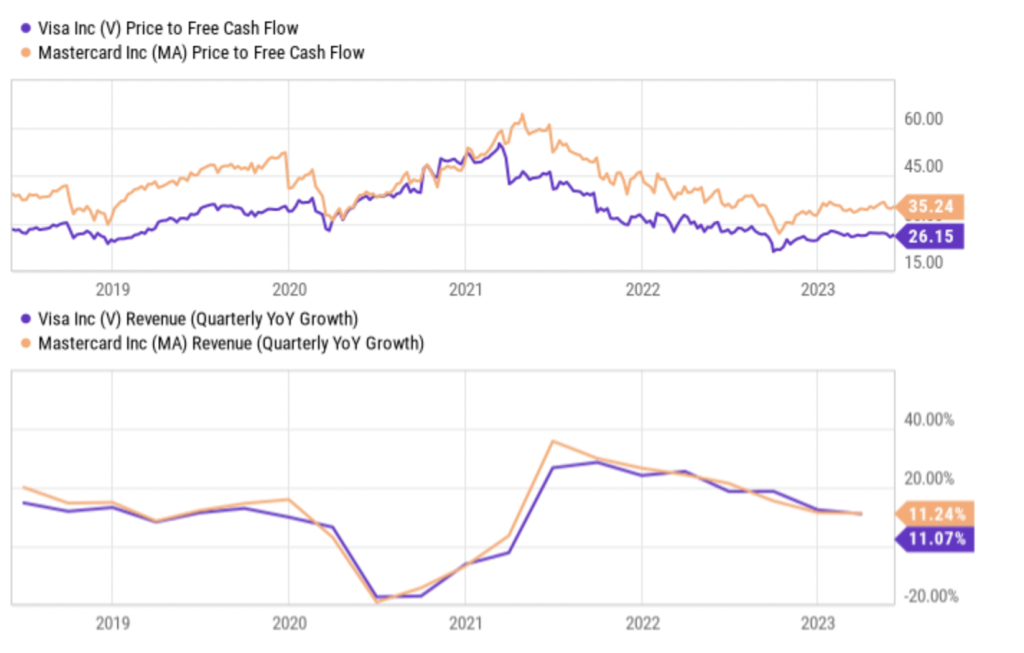

Furthermore, from a valuation perspective, Visa continues to trade at a discount to its duopolistic peer, Mastercard, despite recording similar growth rates.

This means that investors can buy Visa’s growth potential, its free cash flow (FCF) generating prowess, and its rapidly growing and well-funded dividend at a price it hasn’t seen since 2019.

Additionally, the company plows any excess FCF not used to increase its dividend payments into continuous share buybacks. These buybacks have led to the company’s share count declining by 18% across the last decade — further juicing its growth figures.

With annualized revenue and FCF growth of 11% and 17% over the last five years, and paying a growing dividend that only uses 18% of its FCF, Visa is a compounding machine that could pay investors for the rest of their lives.

2. FactSet Research Systems

FactSet Research Systems joined the S&P 500 Index in late 2021. Its financial data and analytics offerings quickly made it a leading competitor in its niche. Since its initial public offering in 1996, FactSet has risen over 11,000%, adding over 7,000 clients and 186,000 users of its products along the way.

FactSet sells to buy-side, banking, wealth, private equity, and venture capital clients. Its workflow areas include research and advisory, analytics and trading, and content technology solutions. Simply put, regardless of where a financial company’s operations lie on the investing spectrum, FactSet has a data and analytics-focused offering to fit them.

Its 98.7% annual subscription value (ASV) retention rate means its financial clients tend to stay for the long term once they are brought into the company’s ecosystem. Furthermore, over 60% of FactSet’s clients use at least one product from each of the company’s three workflow areas — again highlighting the value it provides to its customers.

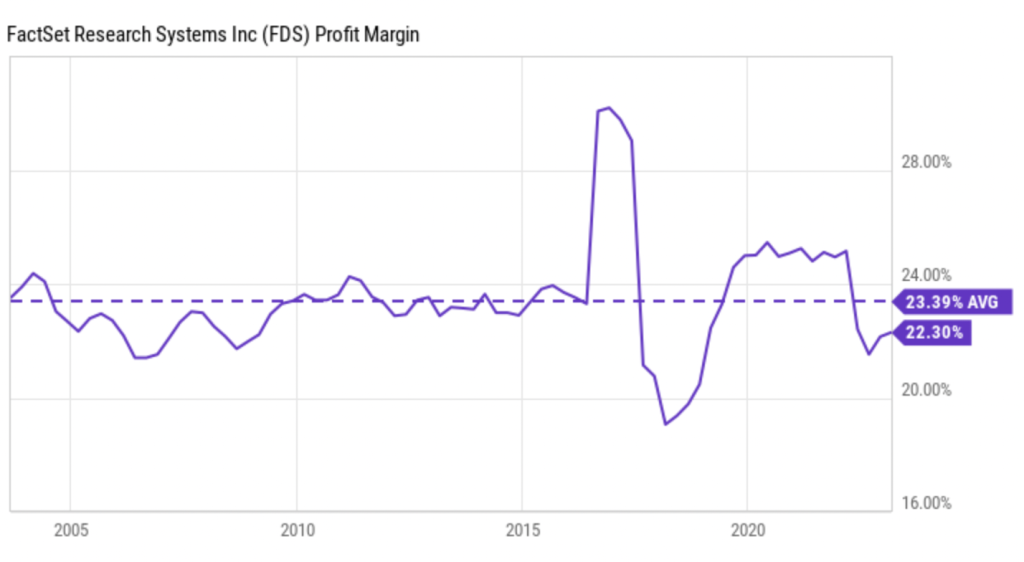

Anchored by its revenue coming primarily from three-year contracts, FactSet sees steady, recurring sales. This helps enable the company to be a natural compounder over the long haul, especially considering its excellent history of net profit margins north of 20%.

While this figure dipped in 2021 as the company integrated its $1.9 billion acquisition of CUSIP Global Services (its largest acquisition ever), it rebounded to a 27% net profit margin in its most recent quarter — well above historical averages.

Armed with this impressive net income margin, FactSet is well-positioned to extend its streak of 23 consecutive years of dividend increases. After growing sales and earnings by 9% annually over the last decade while maintaining a payout ratio of only 24%, the potential future Dividend King should continue increasing its payouts to investors for decades.

3. Nasdaq

Due to consistently drawing many of the most significant new initial public offerings to its exchanges, Nasdaq has delivered a stellar total return of over 500% since 2013.

Despite an extended slowdown in the IPO market, Nasdaq maintained a 91% win rate for U.S. IPOs and attracted 80% of the total capital raised during the first quarter. Thanks to this recognition as the go-to exchange for companies looking to go public, its exchange and its indexes have become synonymous with the worlds of cutting-edge technology and innovative business ideas.

However, Nasdaq’s smallest business segment may add the most excitement to an investment in the company today.

By acquiring anti-financial-crime firm Verafin in 2020, Nasdaq launched full speed ahead into policing the markets. With fraud detection, anti-money laundering, and surveillance across its exchange, Nasdaq’s nascent unit offers desperately needed products in a world where financial shenanigans seem to grow exponentially.

Now counting 2,400 fraud and anti-money laundering clients and 200 surveillance clients, Nasdaq aims for 20% growth annually from the unit for the next three to five years.

Best yet for investors, this promising growth optionality comes with the company’s 1.5% dividend — which only uses 30% of net income. Having raised its dividend for 10 consecutive years, including a 10% jump in its most recent increase, Nasdaq looks like the perfect blend of dividend and business growth that should reward investors for the rest of their lives.