This fast-growing semiconductor company can keep growing at a terrific pace thanks to its massive end market.

Technology stocks have been hammered this year as investors have shunned richly valued, high-growth companies for a multitude of reasons, including rising interest rates, surging inflation, and the Russia-Ukraine war, leading to a 28% slide in the NASDAQ-100 Technology Sector index.

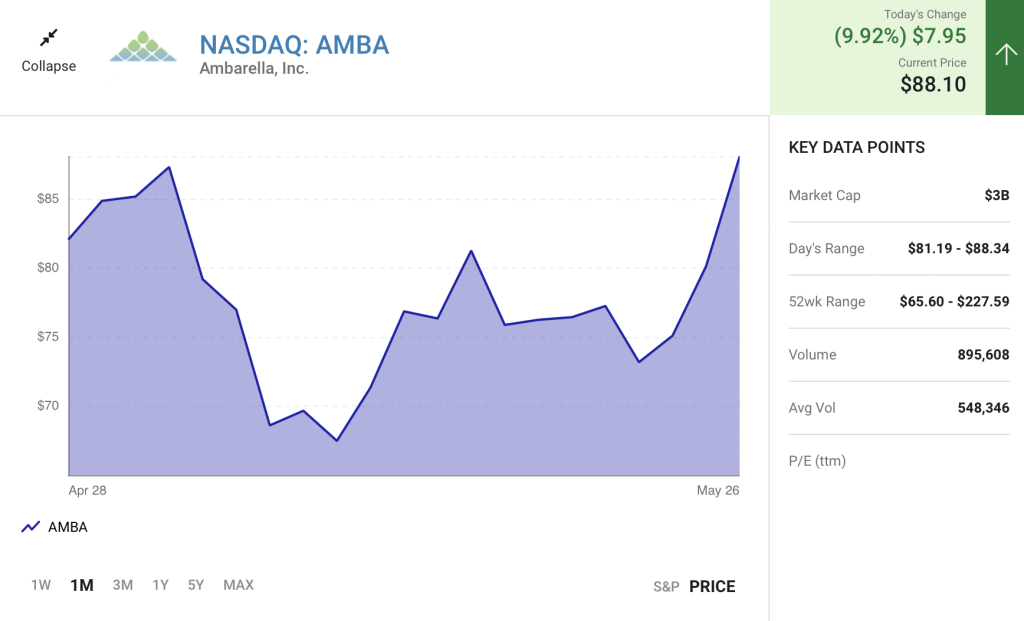

The NASDAQ’s slide has led to a brutal sell-off in Ambarella (AMBA 9.92%) stock. Shares of the chipmaker, which supplies chips used in security and automotive cameras, have crashed 60% so far this year despite the company’s terrific growth. Investors, however, are hoping for a turnaround in Ambarella’s fortunes when it releases its fiscal 2023 first-quarter earnings report on May 31.

But will Ambarella be able to overcome the supply chain problems affecting the semiconductor industry and deliver a solid report? Let’s find out.

Ambarella could deliver healthy growth once again

Wall Street expects Ambarella to earn $0.36 per share on revenue of $90 million in fiscal Q1. The revenue estimate is in line with Ambarella’s top-line guidance of $88.5 million to $91.5 million, which the company issued in February this year. The midpoint of Ambarella’s guidance points toward a 28% year-over-year increase in revenue, while earnings are expected to increase substantially over the prior-year period’s figure of $0.23 per share.

Ambarella had guided for an adjusted gross margin of 63% to 64% in fiscal Q1, which would be an improvement over the prior-year period’s figure of 62.9%. The strong growth in Ambarella’s top line and healthier margins should translate into a robust bottom-line performance and help the company match or beat analysts’ expectations. It is worth noting that Ambarella has easily bested Wall Street’s expectations in each of the last four quarters.

However, there’s one potential headwind that investors may want to keep an eye on. Ambarella warned on its February earnings conference call that a tight supply of 14-nanometer chips from its foundry partner Samsung could later impact its fiscal Q2 revenue to the tune of $5 million.

So the company’s near-term guidance may take a hit on account of the chip shortage that’s plaguing semiconductor companies. Additionally, supply chain challenges could continue weighing on Ambarella if the company isn’t able to secure enough supply to meet demand. Ambarella’s vice president of finance John Young indicated that the earnings call:

Underlying demand remains solid, but supply side conditions are highly dynamic. First, as Fermi [Ambarella’s CEO] indicated, our lead times remain extended, and we are now facing new challenges and uncertainty with regard to our suppliers’ timing of deliveries for our 14-nanometer video processors. Second, some of our customers have experienced significant delinquencies from other component suppliers.

Despite these headwinds, Ambarella management remains upbeat about the company’s prospects in fiscal 2023 and beyond.

Fast-growing markets should ensure long-term growth

Ambarella could step on the gas in the second half of fiscal 2023 once it starts shipping its new computer vision chips based on a 5-nanometer manufacturing process, which are expected to carry a higher average selling price. The company expects computer vision chips to produce 45% of its total revenue this year thanks to the growing application of these processors in various artificial intelligence (AI) based applications spread across various verticals such as automotive, the Internet of Things, and security cameras, among others.

According to a third-party estimate, the market for AI-enabled computer vision could grow at an annual rate of 39% through 2030 and hit $207 billion in revenue, indicating that Ambarella’s end-market opportunity is set to expand at a rapid pace for years to come. As a result, it is not surprising to see why the company’s bottom line is expected to clock a compound annual growth rate of 87% for the next five years, a pace that the company could sustain beyond that as its addressable opportunity increases.

The good part is that Ambarella’s chips have already been selected by several customers to power their computer vision applications, and that should help the company achieve the impressive growth that the market expects. All this indicates why buying Ambarella following its sharp pullback in 2022 could be a prudent long-term bet.

The semiconductor stock is trading at 8.8 times sales, which is lower than its 2021 sales multiple of 24. This gives investors a solid opportunity to get into Ambarella at an attractive valuation before the massive opportunity that the company is sitting on supercharges its stock.