An up to 31% plunge in the Nasdaq is the perfect excuse to put your money to work in these three steady businesses.

It’s been a wild year on Wall Street for the investing community. Since hitting record-closing highs five months ago, the 126-year-old Dow Jones Industrial Average and broad-based S&P 500 each fell into correction territory with double-digit percentage declines.

Meanwhile, things have been even more challenging for the growth stock-focused Nasdaq Composite(^IXIC 0.29%). The index that’s led most rallies over the past decade endured a peak-to-trough intra-day decline of 31% between November 2021 and May 2022. This sizable drop firmly places the Nasdaq in a bear market.

Although there’s no question that bear markets can be worrisome and test investors’ resolve, they’re also, historically, the ideal time to put your money to work. Because most stock corrections resolve quickly, and every notable decline in the market has eventually been wiped away by a bull market rally, buying high-quality stocks during these dips is a smart move.

It just so happens that some high-quality companies also happen to be among the safest stocks investors can buy during the Nasdaq bear market. If you’re looking to put your money to work in highly profitable, time-tested businesses that won’t cause you to lose sleep at night, the following three companies are some of the safest stocks on the planet you can buy right now.

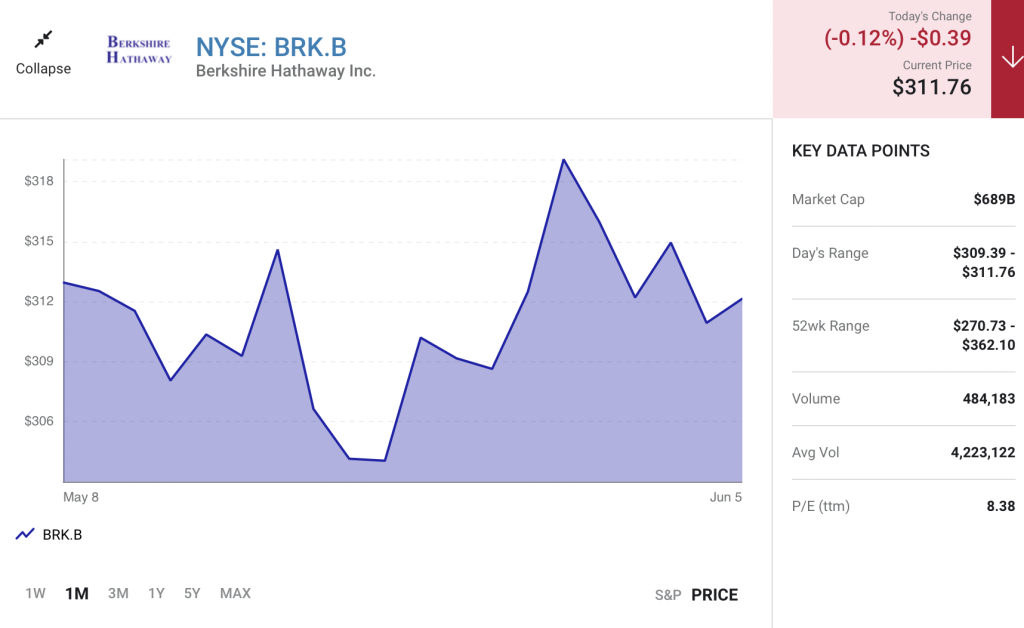

Berkshire Hathaway

The first extremely safe stock investors can confidently buy into is billionaire Warren Buffett’s conglomerate, Berkshire Hathaway (BRK.A -0.01%)(BRK.B -0.12%).

Even though every online brokerage will caution that “past performance is no guarantee of future results,” it’s tough to overlook the Oracle of Omaha’s track record. Since becoming CEO in 1965, Buffett has created more than $680 billion in value for Berkshire Hathaway’s shareholders and led his company’s stock to an average annual return of 20.1%. Over 57 years, an annualized return of 20.1% equates to a gain in the company’s Class A shares (BRK.A) of 3,641,613%!

One of the key reasons Berkshire Hathaway has been so unstoppable for so long is its cyclical focus. The vast majority of investments made by Berkshire, along with the company’s roughly five dozen acquisitions, have been in cyclical companies. A “cyclical” stock does well when the economy is growing and struggles when recessions arise.

What’s important to understand here is that recessions tend to resolve quickly, while periods of economic expansion often last years. By angling Berkshire Hathaway to take advantage of disproportionately long expansions, Buffett is playing a numbers game that will almost certainly work in his (and his shareholders’) favor.

Something you might not realize about Berkshire Hathaway is that it’s a passive-income powerhouse. Although it doesn’t pay a dividend, Buffett’s company is set to collect more than $6 billion in dividend income over the next 12 months (that includes preferred stock income). In fact, 10 dividend stocks are bringing in between $101 million and $904 million annually for Berkshire.

The beauty of dividend stocks is that they’re almost always profitable and time-tested. In other words, they’re companies we’d expect to grow in value over time. Buying and holding groups of high-quality dividend stocks has helped Buffett’s company vastly outperform over the long run.

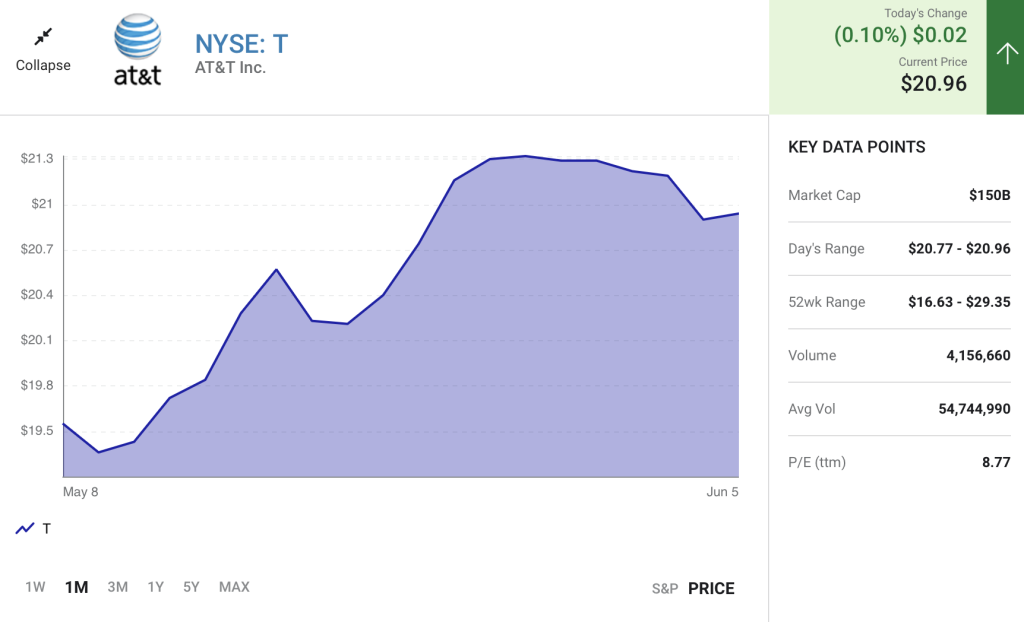

AT&T

A second exceptionally safe stock that’s begging to be bought by investors during the Nasdaq bear market is telecom behemoth AT&T (T 0.10%).

The reason AT&T can help investors sleep well at night is simple: Its revenue and cash flow are relatively transparent and predictable. A smartphone and wireless access have effectively become basic necessities. This would suggest that economic contractions and recessions won’t have much of an impact on the company’s wireless churn rate.

While AT&Ts growth heyday of the 1980s and 1990s is long gone, there’s still a catalyst or two that can move the profit needle steadily higher. At the moment, nothing is more important for AT&T than the 5G revolution.

Over the next couple of years, AT&T will be investing billions of dollars to upgrade its domestic wireless infrastructure to support 5G download speeds. It’s been about a decade since the last major wireless infrastructure upgrade, which suggests we’ll see a steady consumer and enterprise device replacement cycle, and a sizable uptick in data consumption. Data happens to be where AT&T’s wireless division generates its juiciest margins.

The other big catalyst for AT&T was the spinoff of content arm WarnerMedia in April, and its subsequent merger with Discovery to create a new media entity, Warner Bros. Discovery. When this deal closed, AT&T received a $40.4 billion cash payment. This cash, coupled with a reduced base annual dividend, should allow AT&T to put a meaningful dent in its outstanding debt.

It’s also worth pointing out that, even with a reduced annual payout, AT&T is still yielding a hearty 5.3%. This is an inflation-fighting yield from a company valued at only 8 times Wall Street’s forecast earnings in 2022 and 2023.

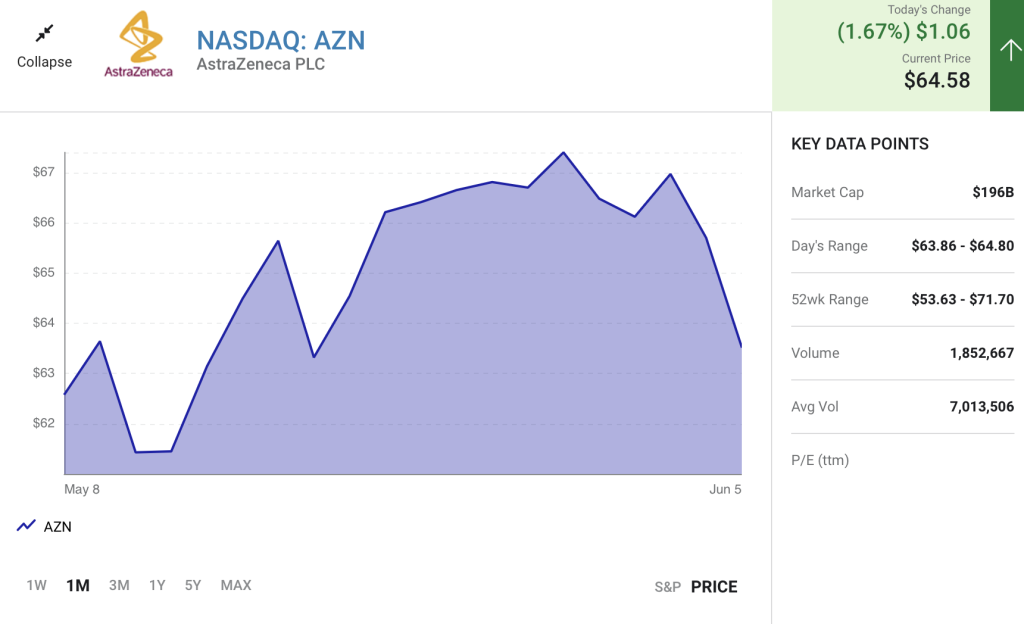

AstraZeneca

A third reliably safe stock investors can buy right now with the Nasdaq in a bear market is pharmaceutical giant AstraZeneca (AZN 1.67%).

Generally, healthcare stocks are a smart place to put your money to work during periods of heightened volatility. No matter how volatile the stock market gets, people are always going to get sick and require prescription medicine, medical devices, and healthcare services. In AstraZeneca’s case, it can take solace in knowing that patients will still need its prescription drugs no matter or how well or poorly the U.S. and global economy are performing.

What makes AstraZeneca such a stellar stock to own is its innovation and capacity to make smart acquisitions.

The company is seeing double-digit percentage growth in most prescription-drug categories. Oncology and cardiovascular, which combine to account for a little over half of net product sales, saw respective constant-currency revenue growth of 25% and 18% in the first quarter (Q1). The company’s blockbuster oncology trio of Tagrisso, Imfinzi, and Lynparza, grew by 11% to 17%, excluding currency changes, in Q1. Meanwhile, next-generation type-2 diabetes drug Farxiga hit $1 billion in quarterly sales (67% year over year sales growth, excluding currency movements). Superior growth from these blockbuster therapies appears sustainable.

The other key growth driver for AstraZeneca is its genius buyout of rare-disease drugmaker Alexion Pharmaceuticals, which closed in July 2021. Rare-disease drugmakers often face little competition for the indications they target, and approved therapies are rarely met with any list-price pushback by insurers.

Something for investors to note is that, before being acquired, Alexion developed a replacement drug(Ultomiris) for blockbuster therapy Soliris, which had been bringing in about $4 billion annually. Ultomiris is administered less frequently than Soliris, and should, over time, absorb most of Soliris net sales. Developing Ultomiris secured Alexion’s — and now AstraZeneca’s — cash flow for probably the next decade.

AstraZeneca is highly profitable, pays out a 2.2% yield, and has no surprises to offer investors. It’s the perfect safe stock to consider buying in a Nasdaq bear market.