These companies have earned brand recognition around the world.

Stock-split fever has swept through the investing world this year, fueled in part by Amazon‘s (AMZN 0.06%)recent 20-for-1 split and Alphabet‘s (GOOG -0.37%) (GOOGL -0.47%) upcoming 20-for-1 split. Why is everyone so excited? Splitting a stock reduces the price per share by effectively creating more shares, which makes the stock accessible to more retail investors. That could translate into price appreciation when the next bull market rolls around.

As a caveat, stock splits have no impact on metrics like revenue growth or cash flow, so they make for a poor investment thesis in the absence of solid fundamentals. Fortunately, Amazon and Alphabet are both high-quality businesses brimming with potential.

Here’s why both stocks are worth buying.

1. Amazon

Amazon is the second -most valuable brand in the world, according to Brand Finance. The company enjoys a leadership position in both e-commerce and cloud computing, and it’s gaining ground in digital advertising. But many investors have overlooked the long-term potential, focusing instead on temporary headwinds like high inflation and rising costs. As a result, the stock is trading at 2.3 times sales, bouncing off its cheapest valuation since February 2016. That creates a significant buying opportunity.

Amazon powered 40% of U.S. e-e-commerce sales last year, and it doubled its fulfillment capacity during the pandemic, further cementing its lead over other retailers. At the same time, Amazon Web Services (AWS) held 33% market share in cloud infrastructure services at the end of 2021, more than Microsoft and Alphabet combined.

Shareholders should be particularly excited about that. AWS is growing faster than Amazon’s retail business, and its operating margin is consistently around 30%, much higher than the mid-single-digit operating margin on retail sales. That cash flow should make Amazon increasingly profitable over time.

Finally, Amazon’s advertising business is taking root across its many digital properties, from its online marketplace to Fire TV streaming platform. In fact, Amazon captured nearly 12% of U.S. digital ad spend last year, and that figure will approach 15% by 2023, according to eMarketer. Like cloud computing, digital ad sales come with higher margins than retail, meaning shareholders actually have two reasons to believe profitability will accelerate.

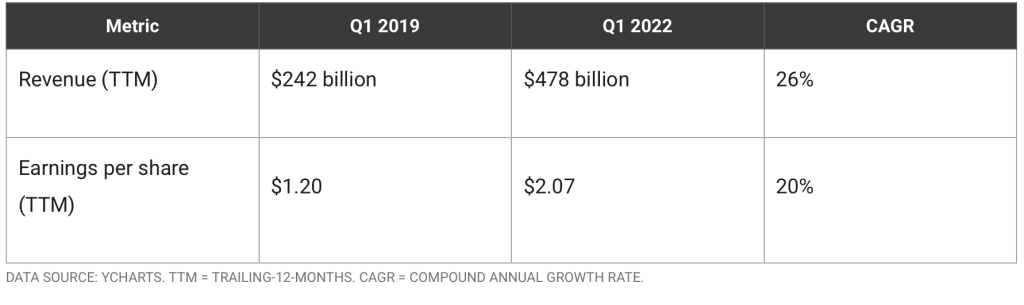

Despite headwinds in the most recent quarter, Amazon has delivered admirable financial results over the past three years.

Looking ahead, investors have good cause to be bullish on Amazon. Online retail sales will grow at 11% annually to reach $7.4 trillion by 2025, and digital ad sales in the U.S. will grow at 11% annually to hit $315 billion by 2025, according to eMarketer. Meanwhile, cloud computing spend will grow at 16% per year to reach $1.6 trillion by 2030, according to Grand View Research. As a key player in all three industries, Amazon looks unstoppable.

2. Alphabet

Alphabet breaks its operations into two segments: Other Bets and Google. Other Bets is a collection of early-stage companies working in cutting-edge fields like autonomous vehicles, quantum computing, and artificial intelligence (AI). And Google is the umbrella term for digital advertising and cloud computing services.

Alphabet has earned the type of brand authority that few businesses can claim. Google Search is effectively the gateway to the internet, holding 88% search-engine market share. YouTube is the second-most-popular streaming service as measured by viewing time, and Google Play is the second-most-popular mobile app store.

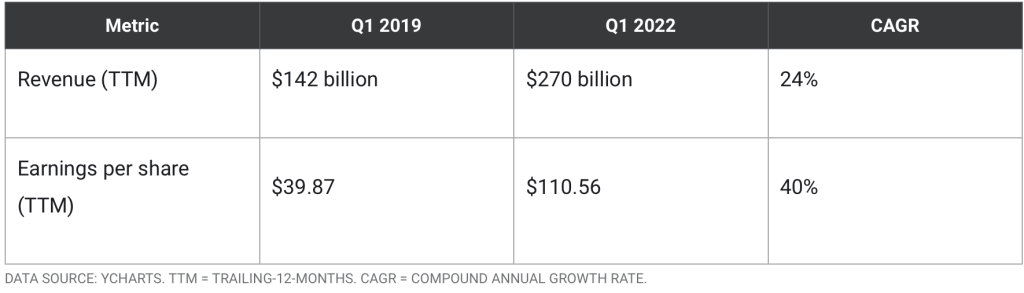

Those content platforms have paved the way to Alphabet’s dominance in digital advertising. Last year, the company captured a jaw-dropping 28% of digital ad spend worldwide, according to eMarketer. That has translated into impressive financial results.

Going forward, shareholders have good reason to be confident. Global digital ad spend will hit $785 billion by 2025, up nearly 60% from $491 billion in 2021. As the industry leader, Alphabet should benefit greatly from that trend, and given the popularity of platforms like Google Search and YouTube, the company is unlikely to lose that edge any time soon.

Additionally, Google Cloud is the third-largest cloud services provider, and it is growing quickly. Revenue climbed 44% in the last quarter, while the operating loss narrowed slightly. Assuming that trend continues, Google Cloud should eventually become a meaningful contributor to Alphabet’s cash flow.

As a final thought, the Other Bets segment could spin out a game-changing business at some point in the future. Alphabet subsidiary Waymo is already running an autonomous ride-hailing network in Phoenix, which could revolutionize transportation. And DeepMind is using AI to predict protein folding, which has positive implications for drug design and environment sustainability. But even if Other Bets comes to nothing, there is a lot to like about Alphabet.