A reasonably small amount of money can go a long way when it’s invested in industry-leading businesses.

Though it can be tough to admit, investing on Wall Street has its ups and downs. Following a year that saw the iconic Dow Jones Industrial Average, broad-based S&P 500, and growth-driven Nasdaq Composite romp to new all-time highs, 2022 delivered a bear market and the worst full-year returns for the Dow, S&P 500, and Nasdaq Composite since the financial crisis.

Thankfully, pain almost always begets opportunity on Wall Street. Even though we’re never going to know ahead of time how much the major indexes will decline during a correction or bear market, history shows us that every notable drop in the stock market is met with an eventual bull market rally. It makes double-digit downside moves on Wall Street an opportune time for investors to pounce.

In addition to having history on their side, investors are also benefiting from changes made by most online brokerages. In recent years, online brokers have abandoned minimum deposit requirements and commission fees. For the everyday investor, it means any amount of money — even $300 — can be the ideal amount to put to work.

If you have $300 that’s ready to invest, and you know you won’t need this money to cover bills or other emergency expenses, the following three stocks stand out as no-brainer buys right now.

Johnson & Johnson

The first magnificent company that’s a no-brainer buy with $300 right now is none other than healthcare juggernaut Johnson & Johnson (JNJ 0.21%), better known as J&J.

Like every single publicly traded company, Johnson & Johnson is contending with its own unique set of headwinds. Litigation concerning its talcum-based baby powder is, arguably, the biggest gray cloud currently hovering over the company. But if investors take a step back, they’d see that J&J should have no trouble settling existing lawsuits from a financial standpoint. In other words, J&J stock underperforming the broader market in 2023 is an opportunity, not a concern.

Throughout this decade, pharmaceuticals should be Johnson & Johnson’s driving force. More than half of the company’s net sales now derive from novel therapeutics. Although there are risks to this strategy, such as brand-name drugs having finite periods of sales exclusivity, the payoff is a notably higher organic growth rate and a much juicier operating margin.

Beyond pharmaceuticals, Johnson & Johnson has its medical-technologies segment to fall back on. As access to preventative medical care improves globally, demand for medical technologies should grow. It’s a segment that should consistently deliver higher operating cash flow when examined over long periods.

Another reason Johnson & Johnson continues to deliver for shareholders is the consistency seen at the top. Since its founding in 1886, J&J has had just eight CEOs. Minimal turnover at the CEO position means corporate strategies and initiatives are being seen through from start to completion.

Lastly, J&J has a balance sheet that even the most conservative investors can trust. It’s one of only two publicly traded companies to receive the highest possible credit rating (AAA) from Standard & Poor’s (S&P), a division of S&P Global. That’s one notch higher than the credit rating (AA) bestowed on the U.S. federal government.

With Johnson & Johnson stock at its lowest forward price-to-earnings (P/E) ratio in more than a decade, it’s the perfect time for value and income seekers to attack.

Okta

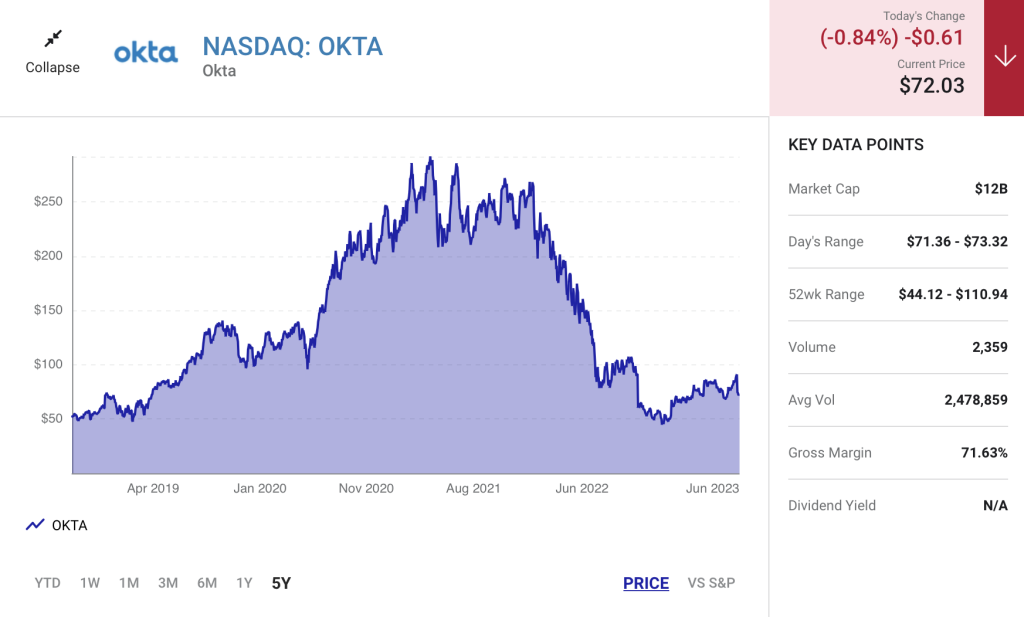

A second no-brainer stock that’s begging to be bought with $300 is cybersecurity company Okta(OKTA -0.84%).

A quick glance at Okta’s chart clearly reveals that Wall Street wasn’t thrilled with the company’s fiscal first-quarter operating results, which were released last week. Shares fell approximately 20% after failing to live up to outsized growth expectations. While double-digit declines are never fun in the short run, they’re just the open invitation investors with cash at the ready need.

One of the reasons Okta stands out as a phenomenal buy is the nature of the cybersecurity industry. With data migration into the cloud accelerating at a rapid pace, third-party providers like Okta are increasingly being relied on to protect sensitive information. No matter how well or poorly the U.S. economy performs, cybersecurity solutions are, effectively, a basic necessity.

Okta makes its home as an identity-solutions provider. More specifically, Okta’s platform is cloud-native, and it relies on artificial intelligence and machine learning to evolve over time. In short, Okta’s platform is enhancing access and observability solutions for businesses utilizing its software-as-a-service (SaaS) solutions, and its platform is becoming increasingly more efficient at recognizing and responding to potential threats.

Despite Okta’s swan-diving following its earnings release, virtually all of the company’s key performance indicators are headed in the right direction. Whereas its total customer count has risen by 69% to just north of 18,000 over the trailing-two-year period, the number of customers generating at least $100,000 in annual contract value has effectively doubled (2,075 to 4,080) over the same stretch. Landing the big fish is important to validating its identity platform and growing its SaaS backlog.

Furthermore, it’s not just new customers that are driving its sustained doubled-digit growth rate. Over the past nine quarters (two years and three months), Okta’s trailing-12-month dollar-based net-retention rate has stuck between 117% and 124%. Put simply, this means existing clients are spending between 17% and 24% more on a year-over-year basis.

The final catalyst for Okta is its acquisition of Auth0, which was completed in February 2022. Despite higher-than-expected integration expenses, Auth0’s pros decisively outweigh its near-term cons. Auth0 opens the door for Okta to push into Europe’s cybersecurity market, which should fuel sustained sales and profit growth.

NextEra Energy

The third no-brainer stock that can confidently be bought with $300 right now is America’s largest electric utility by market cap, NextEra Energy (NEE 1.08%).

The two biggest headwinds facing NextEra are higher interest rates and the ascendence of large-cap tech stocks. The former is a potential issue given that electric utilities often lean on debt-financing for new projects. Meanwhile, the latter is a problem because it’s pulling all interest away from tried-and-true income plays in the utility sector in favor of high-growth tech stocks being driven by the fear of missing out (FOMO). Thankfully, neither of these factors are a particularly big concern for a perennial outperformer like NextEra Energy.

Similar to Okta, NextEra Energy benefits from the predictability of the services it offers. Regardless of what’s going on with inflation or the U.S. economy, demand for electricity doesn’t change much from one year to the next. This consistency of demand allows the company to accurately forecast its annual cash flow and outlay capital for projects and its dividend without worrying about adversely impacting its profits.

To add to the above, electric utilities are almost always monopolies or duopolies in the areas they operate. Though most traditional utilities are regulated by state public utility commissions, they don’t have to worry about competition, price wars, or the volatility of wholesale electricity pricing.

What makes NextEra Energy so special is its focus on renewable energy. As of the end of March, the company was generating 31 gigawatts (GW) of clean energy, including 23 GW from wind power and 5 GW from solar. Both figures are tops globally. Although these clean-energy investments weren’t cheap, NextEra and its customers are now benefiting from lower electricity-generation costs.

Best of all, NextEra Energy isn’t anywhere near finished when it comes to expanding its renewables and storage portfolio. Between the start of 2023 and end of 2026, the company anticipates completing between 32.7 GW and 41.8 GW of green energy projects. This includes bringing up to 19 GW of new solar capacity online.

Conservatively, NextEra believes it’ll grow its adjusted earnings per share by 6% to 8% annually through 2026, as well as increase its base annual distribution by roughly 10% through 2024. Having followed this company for as long as I have, I’ve learned the bar is set low with these forecasts.

The icing on the cake for investors is that NextEra has generated a positive total return for shareholders, including dividends paid, in 19 of the past 21 years. Though past performance is no guarantee of future results, NextEra’s rock-solid foundation bodes well for the patient investor.